Most Australians are in for a shock when they retire due to a lack of planning and preparation.

Hear us out: If you wait until just a few years before you retire or until your home loan is repaid, it can be too late to build a comfortable life for yourself in your retirement years.

Beginner investors may be operating on the advice of parents or peers, who believe that paying off their home loan needs to be prioritised over investment. This approach is outdated and doesn’t guarantee financial freedom.

It’s a risk-averse mindset that may have worked in the past for retirees who could rely on the Age Pension to sustain them through their later years. Unfortunately, with today’s economic environment, this is no longer an option.

Waiting to pay off your home before starting your investment journey leaves you with a shorter investment timeframe. And while paying down the home loan with surplus cash may seem like the low-risk path, it creates a risk of not having built enough retirement savings in the long run.

Here, we take a look at why it’s important to begin your investment journey before paying off your home loan and how you can net more income prior to retirement.

Why you can’t rely solely on the pension

As living costs rise and governments continue to tighten belts, the role of the Australian pension has changed significantly.

As of 2023, the maximum Age Pension payment for singles is $971.50 a fortnight (or $25,259 a year) and $1464.60 a fortnight for couples ($38,079.60 a year).

To be eligible for the payment, a person must be:

- Aged 67 or older, depending on when you were born.

- An Australian resident and have lived in Australia for at least 10 years.

- Meet the income and asset tests.

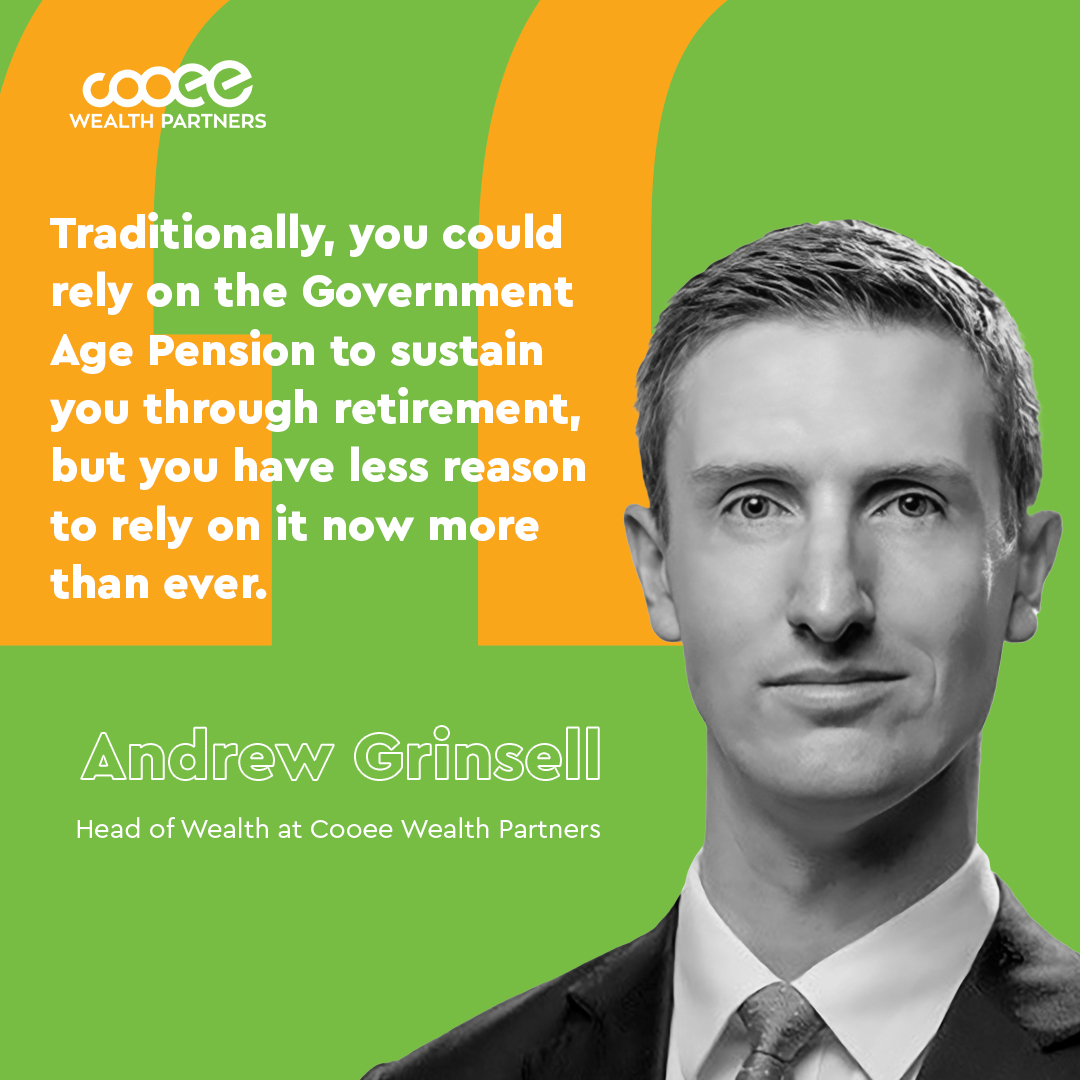

Our Head of Wealth, Andrew Grinsell, says the pension is becoming more of a safety net and less of an entitlement, which is why future-proofing your income should be your focus.

Adopting a complete financial plan is the first step in doing this. Keep in mind that financial planning isn’t simply for the wealthy – it’s for anyone who earns an income, and wants to succeed in life.

“Traditionally, you could rely on the pension to sustain you through retirement, but you have less reason to rely on it now more than ever,” Andrew adds.

“We recommend clients with a long investment timeframe to disregard the Age Pension. If someone is engaging in advice, at a young enough age, they should have enough aspiration to attain a retirement lifestyle that wouldn’t be sustained on a pension.

“Furthermore, they should aspire to achieve adequate wealth to fund this lifestyle, which would see them exceed the relevant age pension thresholds.”

The key is to develop a plan to achieve your goals and the earlier you start, the more likely you are to succeed.

“Creating a plan that builds wealth while you pay off your home loan is a smart move,” Andrew says.

Leaving it too late to invest can leave you with an insufficient timeframe and limited market cycles to build your wealth.

3 ways to invest while paying off your home loan

Generating returns above inflation is the key to building wealth, and the suggestions below are only a few of the ways you can future-proof your finances. Always be sure to create a solid plan with the insight of a reputable financial adviser.

1. Salary sacrifice to super

With good planning and smart choices, your superannuation fund can be a substantial booster for retirement. In addition to compulsory employer contributions, salary sacrifice or personal concessional contributions are two ways to increase your retirement funds – while saving on tax in the meantime.

Salary sacrifice is a great financial arrangement with your employer that allows you to trade a portion of your salary for valuable benefits of similar value. One example is redirecting some earnings into your super fund instead of receiving them as cash. These sacrificed contributions are categorised as employer super contributions, taxed within the fund at different rates depending on the income bracket. People with an adjusted taxable income of less than $250,000 are taxed 15 per cent while high-income earners pay an additional tax called a Division 293 Levy, which results in a contribution tax rate of 30 per cent. Whichever the income bracket, these contribution rates are still more favourable for most people than their marginal tax rate.

Embracing salary sacrifice will optimise your superannuation for your future. It is a tax-effective strategy that your future self will thank you for.

2. Debt recycling

This strategy involves expediting the repayment of non-deductible debts while accumulating wealth through tax-efficient means. Basically, the method revolves around recycling the debt with tax-deductible debt from profitable investments.

One example is to use home equity to invest in income-producing assets with the possibility of growth. Home equity is the difference between the value of your property and the amount you owe the bank. It can also provide an investor with substantial borrowing power – the more equity, the more a bank may lend.

For a debt recycling concept to work, you will a long-term investment mindset as well as:

- A home loan with available home equity.

- Stable and independent income to cover investment loan interest.

- Willingness to leverage debt through an investment loan.

- The ability to feel comfortable with risk and potential short-term investment value fluctuations.

- Contemplation of income protection insurance for added security in case of illness or injury impacting work.

Your wealth partner will be able to work through each of these steps with you.

3. Positive cash flow investments

It’s important to create a portfolio that builds wealth using different types of assets.

We have three examples of how you can generate positive cash flow investments:

- Managed funds allow multiple investors to pool funds collectively and access superior assets that they otherwise couldn’t afford by themselves.

- Money-generating assets including direct residential or some commercial real estate, property-managed funds, high-yield shares and high-yield managed funds.

- Bonds and stocks with dividends can be a great way to earn a passive income.

These investment options can complement the home equity you’ve built with your existing real estate and an additional avenue for you to build wealth as part of your financial and investment strategy.

With living costs continuing to rise and the Aged Pension no longer cutting it in terms of future security, Australians have no choice but to plan wisely for the future with smart, well-planned investments.

Investments can be used to help clear the mortgage; when you build wealth and achieve returns higher than you would’ve gotten from paying down debt, you get ahead. Book a meeting with one of our wealth partners to review your options and see where you can achieve positive returns.